Markets

New Oriental Education Making a Comeback?

|

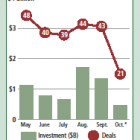

China-based shell merger company New Oriental Education & Technology Group (EDU) took an anvil ride in July, when a Muddy Waters report questioned many of the company's claims. The company's shares fell 35% when the report was released on July 18, but more recently positive news, including regulatory approval of consolidation accounting, has New Oriental on the uptick. Share prices moved up on Oct. 15, when New Oriental, which bills itself as the largest provider of private educational services in China, announced that Securities and Exchange Commission staff voiced no objection to the accounting behind merging some business units into the company's consolidated financial statements. The SEC's approval of accounting practices is, of course, hardly an endorsement of the company or its stock. But the news did bring on a flurry of trading after New Oriental shares opened at $19.34 on Oct.